Buy Now Pay Later solutions boost furniture e-commerce conversion by up to 30%. Learn how flexible payment options are reshaping purchasing decisions in Poland's furniture market.

Buy Now Pay Later — the model that lets customers order now and settle later — is reshaping the rules of furniture sales in Poland. Industry estimates indicate that offering flexible payment methods increases conversion rates in furniture e-commerce by 20–30%. For custom furniture producers such as Grandis Trade, this signals a clear priority: how a purchase is financed often matters more than the sticker price itself.

The Psychology of High-Ticket Purchases — Why Furniture Is Different

Furniture is both an emotional and a financially significant decision. A customer who needs a new kitchen or wardrobe system faces a genuine dilemma: the project is compelling, but a bill of several thousand zlotys triggers natural decision-making resistance. The higher the total, the longer the deliberation period — and the greater the risk of an abandoned enquiry.

This is precisely where BNPL acts as a catalyst. Instead of asking «Can I afford this right now?», the customer starts asking «Can I afford the first monthly payment?». That psychological shift lowers the entry threshold and compresses the sales cycle. From our experience across more than 800 residential projects at Grandis Trade, clients who see instalment options at the quoting stage are significantly less likely to scale back an ambitious design in favour of a cheaper, off-the-shelf alternative.

The effect is further reinforced by the ability to physically check the product at home before the final payment is due — something traditional bank credit arrangements never offered.

What Is BNPL and Which Models Are Available in Poland

BNPL (Buy Now Pay Later) is a family of financial services that allow a buyer to defer or spread a payment without going through a formal consumer credit application. The Polish BNPL market has grown rapidly, and several main formats now operate here:

- 30-day deferred payment — the customer orders, receives the goods, tests them at home, and pays only after one month (or returns without financial penalty). This model is especially attractive for upholstered furniture and sofas, where checking colour and firmness in a real interior is critical.

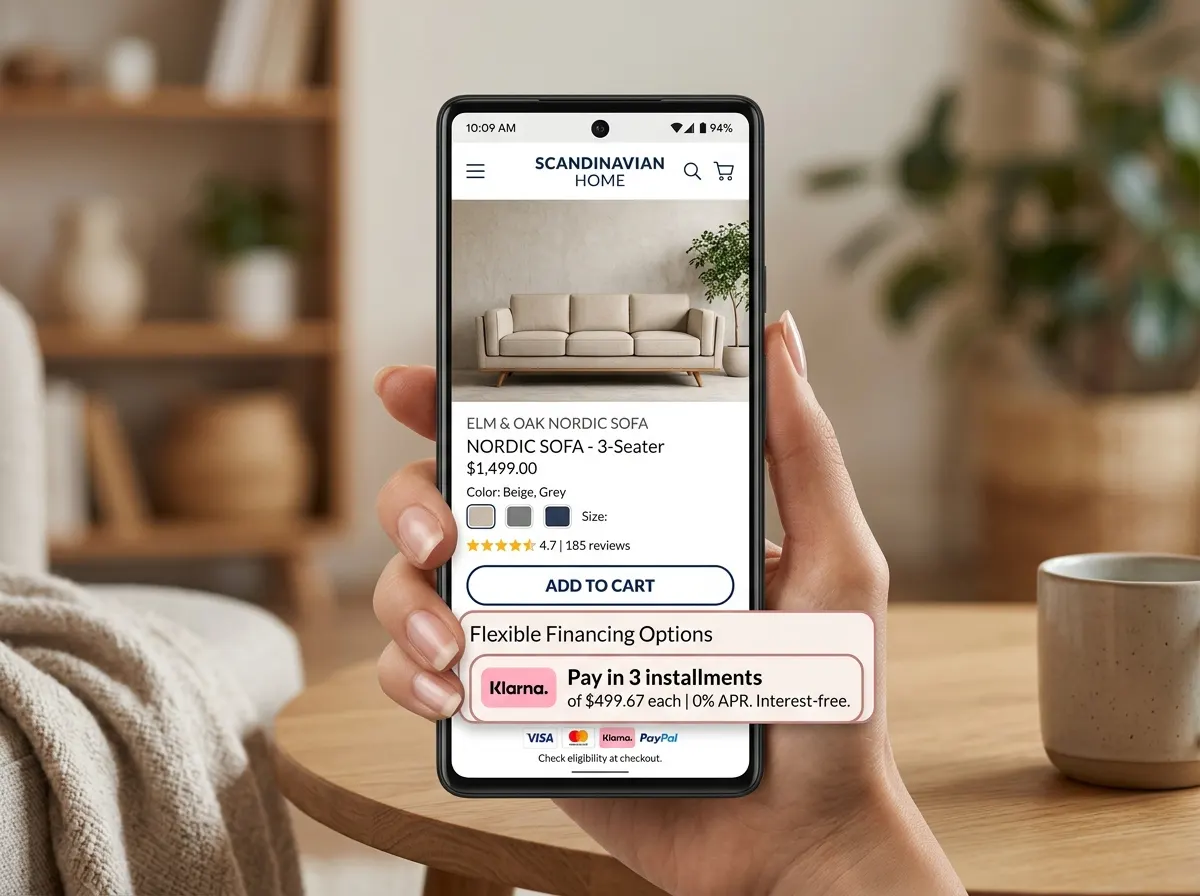

- 0% instalments — the total is divided into 3, 6, 10 or 12 equal monthly payments with no interest. According to consumer market research, zero-interest instalments are the decisive factor when choosing a retailer for more than half of furniture buyers in major Polish cities.

- Interest-bearing instalments — a standard instalment loan handled by the seller's financial partner. Still popular for large projects, though BNPL is steadily displacing it in the segment below PLN 15,000.

- BNPL virtual credit card — solutions combining a revolving credit limit with a flexible repayment schedule, operating entirely within mobile applications.

Each of these models targets a different customer group and a different type of furniture project — from a single wardrobe to a complete apartment fit-out.

BLIK and Localised Payment — the Foundation of Polish E-Commerce

Poland is one of the few European markets with such high adoption of a national mobile payment system. BLIK is effectively the default standard — its usage grows at double-digit annual rates, and its absence from a checkout can mean losing a substantial share of mobile orders.

This has a direct bearing on online furniture shops and configurators. A customer who designs a kitchen on a laptop will often complete the order on a smartphone — and expects BLIK as the final step. The absence of this option is felt as a barrier, not a neutral missing feature.

From the perspective of a custom furniture producer who offers online quotes and accepts digital deposits, BLIK integration is not a nice-to-have but a prerequisite for a smooth sales process. At Grandis Trade we work to ensure that the payment step never blocks the design step: a customer can submit a B2C order form or a B2B brief and select a convenient payment method for their deposit.

How BNPL Affects Custom Furniture Sales — Market Specifics

Custom furniture has its own financial logic: a customer typically pays a deposit — usually 50–60% of the total — before production begins, and the remainder on installation. This model differs from standard e-commerce and requires BNPL to be adapted accordingly.

Producers who have integrated deferred payment into the quoting and contract-signing process report — based on our industry experience — a clear increase in average order value. A client who originally planned only a bedroom wardrobe will often add a bed with storage when they see that the instalment difference is only PLN 80–100 per month.

The scale effect matters in B2B as well: when furnishing a restaurant or an office involves tens of thousands of zlotys, spreading payment over 6–12 months is often a prerequisite for signing the contract at all. Smaller companies lack the free capital for a full upfront payment, but their regular cash flow allows them to service monthly instalments. Grandis Trade offers commercial project financing with contract prices fixed in writing and no addenda — which, combined with a flexible payment schedule, removes the main decision barriers for B2B clients.

Payment Model Comparison — Decision-Maker Reference Table

| Payment model | Typical purchase value | Main advantage | Best for | Conversion impact |

|---|---|---|---|---|

| One-time payment | up to PLN 3,000 | No extra formalities | Cash buyers | Baseline |

| 30-day deferred payment | PLN 2,000–10,000 | Try the product before paying | Cautious buyers, first online purchases | +15–20% |

| 0% instalments (3–12 months) | PLN 5,000–20,000 | No financing costs | Budget-conscious buyers | +20–30% |

| Interest-bearing instalments | above PLN 15,000 | Available for higher amounts | Complex B2C and B2B projects | +10–15% |

| B2B invoice financing (30/60/90 days) | above PLN 20,000 | Matched to business cash flow | Companies, developers, HoReCa | Critical for segment |

Conversion impact figures are based on industry estimates and Grandis Trade's experience across more than 800 B2C projects and 300+ commercial fit-outs.

7 Steps to Effective BNPL Integration in Furniture Sales

- Show payment options early — at the configurator or quoting stage, not only at checkout. A customer who sees «from PLN X/month» from the start perceives the project value differently.

- Explain terms simply — «30 days, no interest, no hidden charges» is more readable than a financing policy document. A short message alongside the price eliminates uncertainty.

- Integrate BLIK as the default mobile method — every step of the deposit payment flow must work smoothly on a phone, as customers increasingly finalise orders away from a desktop.

- Match the model to the segment — B2C needs BNPL and 0% instalments; B2B expects deferred invoices and a fixed price locked into the contract.

- Test price communication — «wardrobe for PLN 4,800» versus «wardrobe from PLN 400/month» describes the same product but creates a different perception of affordability. Instalment messaging lifts conversion on high-value items.

- Simplify the verification process — lengthy credit application forms kill conversion. Good BNPL platforms make decisions in seconds, without paper documents.

- Measure the impact on basket value — not just conversion, but average order value. BNPL often improves both simultaneously, because customers opt for full-scope projects rather than cut-down versions.

BNPL and Custom Furniture — Grandis Trade Case Study

A client from the Wola district of Warsaw, owner of a 68 m² apartment, contacted Grandis Trade needing a wardrobe and a kitchen. Initial budget: PLN 12,000 for both. After the first design consultation, the quote for a full sliding-door wardrobe system and a kitchen with an island came to PLN 21,500 — nearly double the original limit.

The client was clearly engaged with the design but hesitated over the budget overrun. When presented with a 12-month zero-interest instalment option, the monthly payment proved manageable — roughly equivalent to what the client had been spending on storage rental for belongings from a previous flat.

The project went ahead. The sliding wardrobe in U2/E1 laminated board and the lacquered-front kitchen were completed within the standard production timeline. The client's review noted that without the instalment option, the outcome would likely have been «a cheap flat-pack wardrobe».

More completed projects from Wola and surrounding Warsaw districts are available in the Grandis Trade portfolio gallery. If you are planning a similar transformation, start with the short B2C form — a free quote and free on-site measurement within 48 hours.

BNPL and Consumer Protection — Regulations in Practice

The rapid growth of BNPL has attracted regulatory attention. The EU Consumer Credit Directive (CCD2) has come into force and brought certain BNPL services under disclosure obligations comparable to consumer loans. For buyers this is good news — greater transparency and protection. For sellers it means verifying that the BNPL platforms they integrate comply with current legislation.

In practice, reputable platforms operating in Poland align with EU requirements, providing full information on costs and cancellation rights. A customer buying custom furniture with BNPL should receive a clear repayment schedule before signing the contract — and good furniture companies already enforce this.

It is also worth noting the debt angle: BNPL lowers the entry threshold for a purchase, but does not relieve the customer of repayment responsibility. Transparent communication from the seller — «this is a credit arrangement, you repay PLN X over Y months» — builds trust and reduces misunderstandings later.

BNPL in the B2B Segment — Furniture for Offices, Hotels and Restaurants

BNPL is not reserved for private customers only. In the B2B segment it increasingly appears as deferred invoice payment terms (30, 60 or 90 days) or purchase financing through specialist factoring platforms.

For a restaurant owner furnishing a venue for PLN 80,000–150,000, the ability to pay after opening — once operational revenue has started to flow — is often a prerequisite for the project to go ahead at all. Similarly, a developer finishing 20 rental apartments needs a payment schedule aligned with project phases, not a single consolidated invoice.

Grandis Trade delivers B2B projects for retail chains, hotels, offices and hospitality venues across Warsaw. From more than 300 completed commercial fit-outs, we have found that a flexible financing model shortens the time from brief to signed contract by several weeks — because the client does not need to wait for budget release. We invite you to submit a B2B project brief.

How to Choose a BNPL Platform for a Furniture Business

Selecting the right BNPL platform for a furniture producer or distributor requires weighing several key criteria:

- Transaction limit — custom furniture frequently runs from PLN 5,000 to PLN 30,000. Not every BNPL platform operates at these values; some cap out at a few thousand zlotys.

- Credit decision speed — a customer filling in a form expects a fast answer. Platforms that decide in seconds have a clear conversion advantage.

- Integration with the sales system — BNPL must work seamlessly within the quoting and contract-signing process, not as a separate step that takes the customer outside the main flow.

- Regulatory compliance — the platform must meet CCD2 and Polish consumer law requirements. Before integrating, verify certificates and licences.

- Merchant cost — the BNPL platform commission (typically 1.5–4% of transaction value) should be built into the margin, not discovered after go-live.

Frequently Asked Questions

Is BNPL available for custom furniture orders?

Yes. An increasing number of custom furniture producers and distributors integrate BNPL into the ordering process. For made-to-measure furniture the most common approach is 0% instalments on the deposit, or splitting the total into phases (deposit plus payment on installation), financed through a BNPL partner.

What order values does BNPL cover in Poland?

It depends on the platform. Most popular services cover purchases up to PLN 10,000–15,000. For more expensive projects, bank instalment loans or B2B invoice factoring are available. For projects above PLN 20,000 it is worth negotiating payment terms directly with the furniture producer.

Are 0% instalments truly free?

For the consumer — yes, provided payments are made on time. The financing cost is borne by the seller in the form of a platform commission. For this reason, reputable sellers build this cost into their margin rather than adding it as a surcharge when the customer selects instalments.

Can BLIK be used when ordering custom furniture?

Yes — BLIK is available as standard for online deposit payments. A customer ordering custom furniture online can pay the deposit via BLIK and settle later stages by bank transfer or instalments. The absence of BLIK at the online payment stage is one of the leading causes of abandoned orders.

How does BNPL affect the order value for custom furniture?

Based on industry observations and Grandis Trade's experience across B2C projects, clients using instalment financing tend to choose higher-grade materials and expand their project scope. The result is an average basket value 15–30% higher than for customers paying in full upfront.

Is BNPL safe for a furniture buyer?

Yes, provided the customer uses certified platforms operating in accordance with the CCD2 directive. Before signing a BNPL agreement, the buyer should read the repayment schedule carefully and understand the early repayment conditions. When buying custom furniture, a written contract with the producer specifying delivery timelines and scope provides an additional layer of protection.

Does Grandis Trade offer instalments or deferred payment?

Grandis Trade works with flexible financing models tailored to each individual project. The details are discussed during the quoting stage. We invite you to complete the B2C enquiry form or the B2B brief — we will respond promptly and present the financing options available for your project.

How long does a custom furniture project take at Grandis Trade?

The standard lead time from contract signing to installation is approximately three weeks. A free on-site measurement is carried out within 48 hours of the request, and a 3D design is included in the price. We deliver projects in Mokotow, Wola, Wilanow, Ursynow, Praga, Bialoleka, Bemowo and Zoliborz — more examples are available in the project gallery.

Article last updated: 20 May 2026